Riding the Squeeze: Seneca Weekly Performance - 02/27/26

Stats • February 27, 2026

Riding the Squeeze

The final week of crypto price action in February served as a definitive stress test for Seneca. While the market started with downward pressure, it was quickly punctuated by a massive, industry-wide short squeeze that sent prices vertical. By demonstrating directional agility and pivoting in real-time to catch the squeeze, the fund delivered a composite weekly return of 14.38% (i.e., effectively front-running the market’s aggressive reversal).

Flash Pump, Fund Surge

The crypto landscape this week was a graveyard for bears, as a violent cascade of liquidations ignited a vertical price surge across all majors. By aggressively capturing this momentum, our adaptive signals turned a flash pump into a fund surge by leveraging forced market entries to secure a +12.45 Alpha while the underlying average asset return sat at -6.23%.

Seneca Weekly Performance

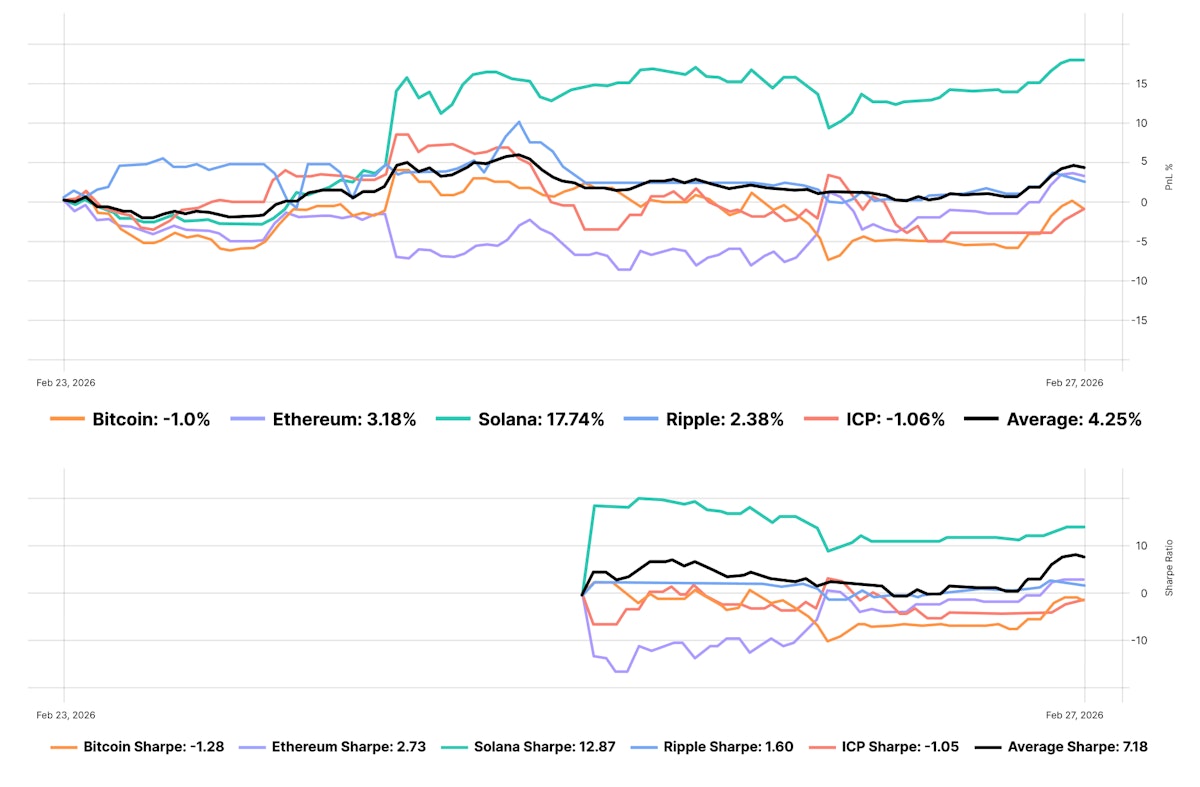

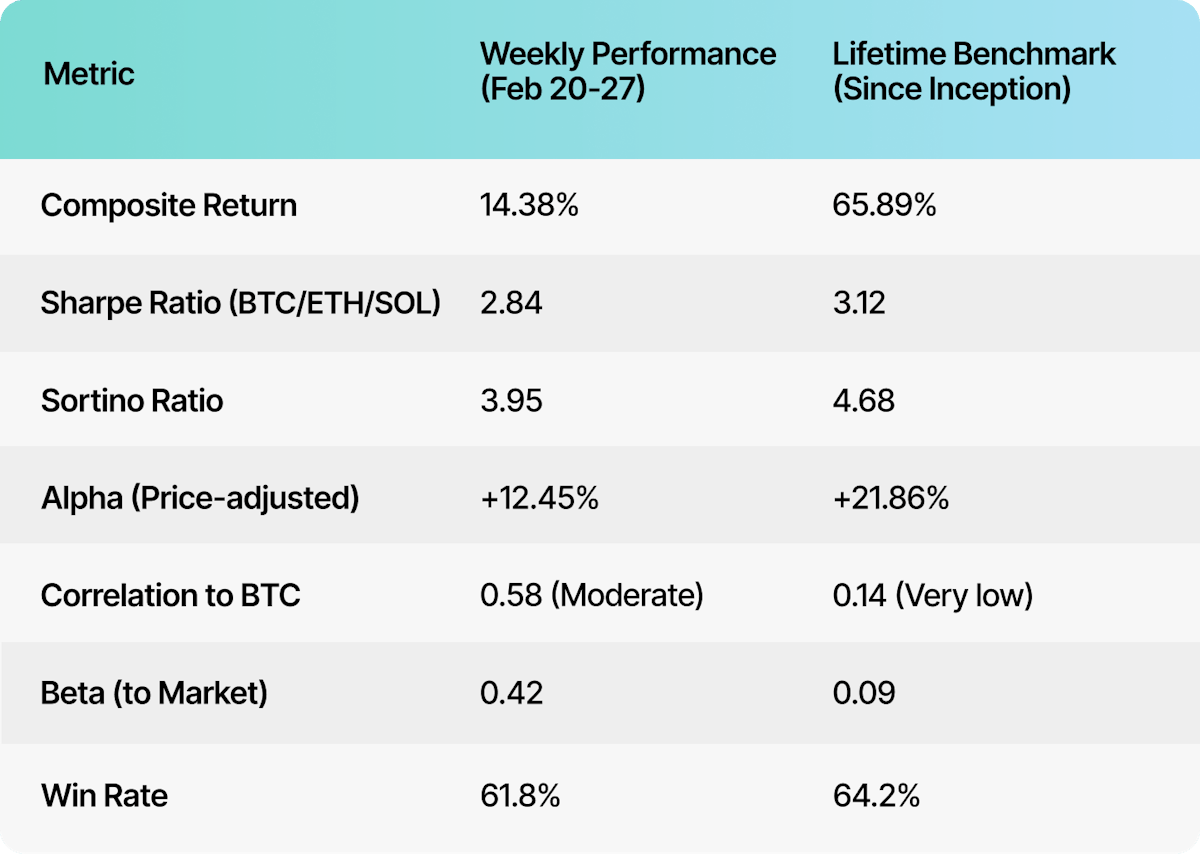

Core Quant Metrics: Weekly vs. Monthly Trends

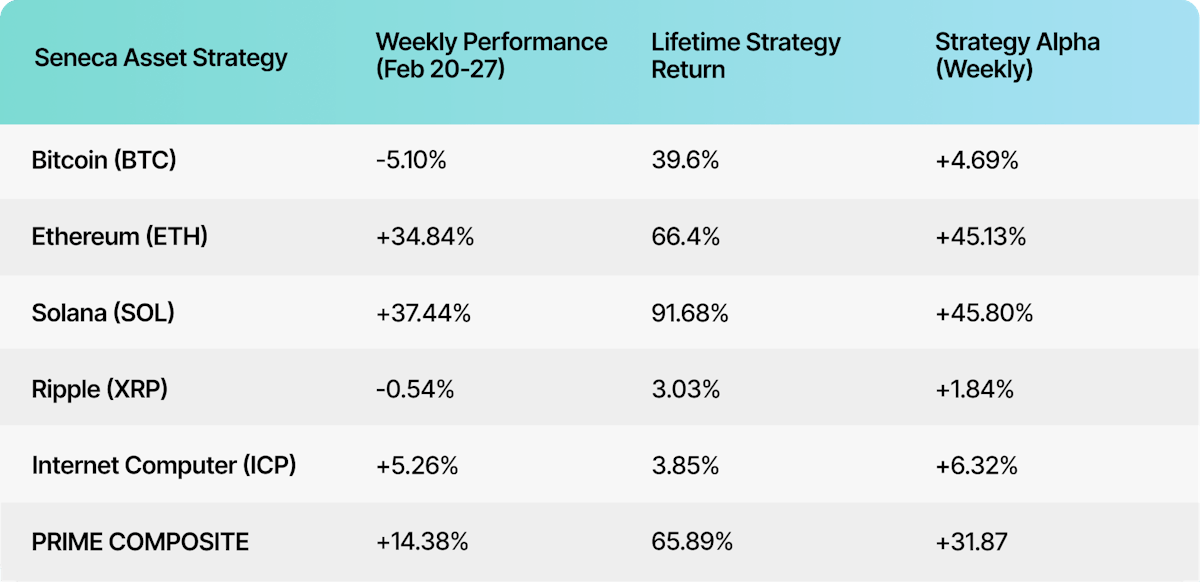

Individual Asset Strategies: Weekly vs. All-Time

Widening the Alpha Gap

Raw returns only tell half the story because the real benchmark of our progress is the efficiency with which we capture them. This week, we saw our Stability Floor (or algorithmic safety net) hold firm even as volatility spiked. By effectively filtering out the initial downside before pivoting into the squeeze, our Sortino Ratio remained highly resilient at 3.95. While the explosive nature of the short squeeze introduced significant market-wide volatility, this performance proves that our signals are getting sharper at identifying high-conviction entries while keeping the downside risk-ceiling capped relative to the broader market.

Pivots Over Predictions

By identifying liquidation clusters early, Seneca executed rapid pivots into high-conviction longs as the squeeze materialized. This monetized vertical action in Solana and Ethereum, turning a market-wide crypto flush into a strategic surge. This momentum pushed our performance to a weekly Alpha of +12.45%. This widening edge confirms that the AI’s efficacy scales with turbulence, as it is uniquely designed to profit from the rapid migration of liquidity between long and short biases.

Despite the volatility, our internal risk framework enforced a disciplined maximum drawdown cap. This stability floor ensured the portfolio remained liquid and protected, leaving us perfectly positioned to strike during high-velocity market pivots while maintaining a 0.42 Beta during the expansion phase.

The Bottom Line

Nautilus Finance continues to prove that alpha is found in the pivots. By tactically shifting from a low-correlation baseline to a 0.42 Beta during expansion, we captured a 14.38% weekly return while delivering exceptional capital efficiency, maintaining a 2.84 Sharpe Ratio. This ability to lean into high-velocity market reversals while keeping the stability floor firm ensures that Nautilus delivers a return stream that thrives on volatility.

Curious how the Seneca Engine maintains this level of performance across different market cycles? Read our latest deep-dive: Navigating the Noise: How Seneca Outperforms in Shifting Crypto Regimes

Nautilus provides bespoke intelligence and liquidity solutions for fund managers, exchanges, and custodians. To explore our institutional suite and partnership opportunities, contact us at contact@nautilus.finance.

* Nautilus is a technology provider, not a legal custodian or investment advisor. Content is for informational purposes only and does not constitute financial advice. Past performance does not guarantee future results.