Quant Trading Is Not One Thing. And Neither Are We.

Perspectives • March 19, 2026

Q1 2026 exposed a structural problem across quantitative trading. Here is what separates an adaptive intelligence engine from a model that simply stops working when the regime changes.

The Pattern Most Quants Missed

In the first two weeks of 2026, US quant funds lost an estimated 2.8% per UBS prime brokerage data, marking the largest single-day deleveraging event since late December. Man Group, Two Sigma, Point72's Cubist unit, and Renaissance all drew down as crowded factor positions unwound simultaneously. Goldman attributed the losses to three causes: crowded long books, adverse short squeezes, and idiosyncratic moves that systematic models had no feature to anticipate.

February compounded it. Iranian military escalation pushed oil past $108 recently, the Fed held at 3.5-3.75%, and BTC drew down by over 50% from cycle highs. Risk assets moved together in ways that broke standard allocation assumptions across traditional and crypto portfolios alike.

Igor Tulchinsky, founder of WorldQuant, framed the opportunity plainly: "We can use AI and LLMs to transform and discover alphas across different domains." And: "We trade the ripples, not the waves."

A Category Problem with Consequences

"AI quant" is applied to a wide range of things that don't behave the same way under pressure: momentum bots, factor models designed for 2008 equity markets, neural networks trained on three years of crypto bull cycle data. Over 70% of hedge funds now use machine learning somewhere in their process, but only around 18% rely on it for more than half of their signal generation. Most are running historical-pattern systems with an AI label on top.

Traditional quant models operate on one assumption: that statistical properties of markets are stable enough for historical patterns to repeat. In calm, trending regimes, that approach has edge. In regime breaks, it goes silent. The model isn't wrong about history. It simply has nothing to say about a market that has moved outside its training distribution.

Why Context is the Signal

The Transformer architecture at its core reads market data the way a language model reads text: not sequentially, but holistically. Every signal is weighed against every other signal simultaneously. A funding rate spike means something different when oil is above $100 and equity vol is expanding than it does in a calm risk-on environment. Our system is built to know the difference.

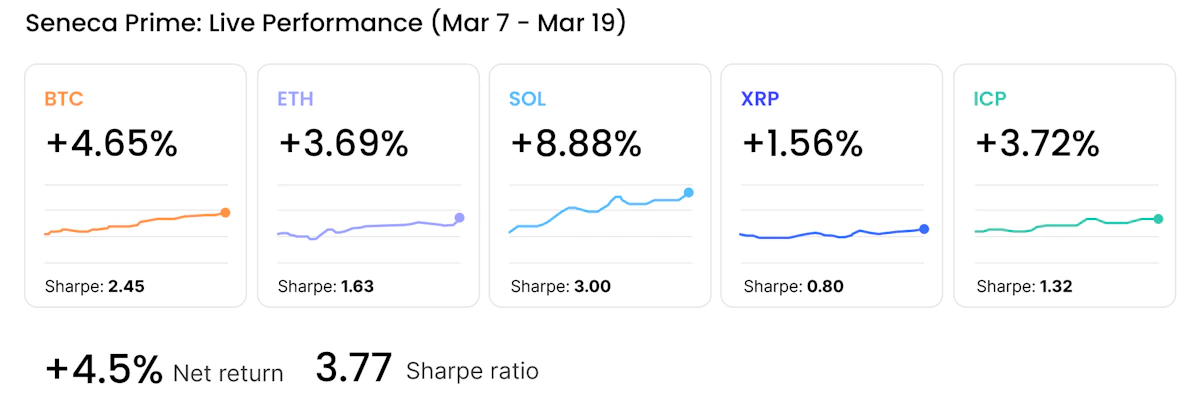

What the Past Two Weeks Show

We do not publish analysis without showing the underlying results. Here is where our live strategies stood for the period March 7 through 19, 2026, one of the most dislocated macro environments of the quarter.

A portfolio Sharpe of 3.77 across a period that included geopolitical escalation, Fed paralysis, and cascading crypto liquidations reflects the core design principle: capital preservation and directional accuracy are not competing objectives. Our pre-trade risk management layer reduces or reverses exposure when market conditions deteriorate, before hard stop- losses are triggered. During the January to February drawdown, our strategies restricted losses to approximately 7% while Bitcoin fell 34%. That differential compounds.

Regime Change Breaks Most Models

The February escalation shows how geopolitical shocks propagate through crypto. Iranian military action didn't reprice Bitcoin fundamentals. It compressed institutional risk tolerance. Leveraged longs, already stretched from January momentum trades, hit risk limits simultaneously as oil spiked and equity futures dropped. The resulting liquidations cascaded through perpetual markets via second-order deleveraging that no crypto-specific model was built to anticipate.

Both momentum and mean-reversion models failed. Not from poor signal construction, but because the regime had shifted and neither had the architecture to detect it. The same failure hit Man Group, Two Sigma, and other large systematic shops in January: crowded assumptions, no regime detection, reactive deleveraging after the damage was done.

Our intelligence engine encodes not just what is happening, but when in a cycle it is happening and how anomalous that moment is. When volatility spikes and funding rates diverge from price action simultaneously, that's a regime signal. The Adaptive Positional Encodings are built to weight that signal correctly and act before the cascade.

Questions Worth Asking Your Signal Provider

The volatility of Q1 2026 is a useful moment to ask a few questions that distinguish what a quantitative system actually is from what it claims to be.

Does your model understand when something is happening, not just that it is happening?

Most quant models treat every signal with equal weight regardless of where it falls in a market cycle. A volatility spike on day three of a liquidation cascade is structurally different from one at the start of a momentum run — but a static model has no way to know that. The same is true of a geopolitical shock: when an exogenous event like a military escalation drives institutional risk-off behavior, the downstream volatility in crypto markets is not organic — it is second-order deleveraging triggered by forced selling elsewhere. A model without contextual awareness will either hold through the deterioration or exit too late.

Does your model distinguish between types of volatility?

Volatility from a scheduled Fed announcement behaves differently than volatility from an unscheduled military escalation. One is anticipated and typically mean-reverts within hours. The other is exogenous and can sustain directional pressure for days. A model that treats both identically will be miscalibrated in geopolitical environments. Contextual intelligence weights the timing and nature of volatility events, not just their magnitude.

What is your drawdown profile when markets are driven by forced selling?

In liquidation cascades, price action reflects forced selling, not fundamental value. Passive and long-biased strategies absorb those drawdowns involuntarily. A system with a genuine pre-trade risk layer detects loss-of-confidence conditions and reduces or reverses exposure before hard stop-losses trigger. During the January to February drawdown, our strategies restricted losses to approximately 7% while Bitcoin fell 34%.That differential compounds.

Is your model getting better, or just getting older?

A static model trained in 2023 has no experience of 2026 market conditions. It has never traded through an Iranian escalation cycle, a 5.5% Fed funds environment, or the specific deleveraging dynamics of institutional crypto positions unwinding simultaneously. A system with continuous genetic optimization evolves asset-specific model variants in real time, selecting the highest-performing configurations for live deployment. The model trading today should be shaped by the conditions it has actually encountered, not the environment it was initialized on.

The Distinction Always Matters

Nautilus is a quantitative intelligence firm. Seneca is the engine at its center: Transformer-native, regime-aware, and deployable across assets, funds, exchanges, and protocols. We are not a single-strategy system. We are the infrastructure layer for AI-driven markets. The quant shop that define the next cycle won't be those with the best discretionary traders. They'll be those with the best intelligence infrastructure. Those are the "ripples" Tulchinsky pointed to. It is what we have built.

Nautilus provides bespoke intelligence and liquidity solutions for fund managers, exchanges, and custodians. To explore our institutional suite and partnership opportunities, contact us at contact@nautilus.finance.

Sources: UBS prime brokerage data, January 2026; Goldman Sachs prime services, January 2026; Hedgeweek, January 2026; MSCI factor crowding analysis, 2025; HedgeThink, November 2025; Forbes/Varchev Finance, May 2025; Nautilus live trading data, March 2026

* Nautilus is a technology provider, not a legal custodian or investment advisor. Content is for informational purposes only and does not constitute financial advice.